Regional hotel property focus: London

London is a major metropolitan area with a depth and complexity far beyond an average city. By numerous measures, London is in effect a region with several large sub-cities, displaying quite distinct market fundamentals. London should therefore not be simply assessed as a single market.

In a hotel sector context, this is perhaps even more obvious when you consider that London accounts for over one in five UK hotel rooms and currently has a supply of around

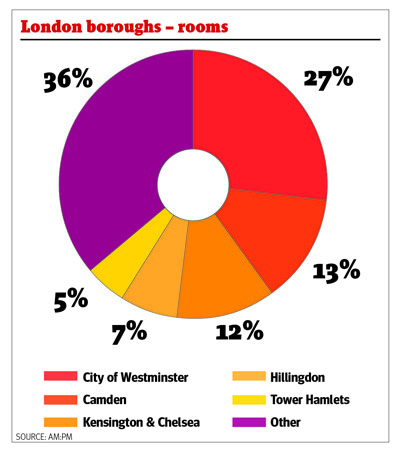

135,000 rooms, which is greater than the combined total supply of Scotland and Ireland.

The City of Westminster in turn is the largest hotel market in London, where it has more rooms than the major UK regional city markets of Birmingham, Liverpool and Manchester added together. Hillingdon, which includes much of the Heathrow market, has more rooms than Glasgow. There are a further five London boroughs with hotel supply of 5,000 rooms or more, which is the hotel market equivalent of Bristol or Cardiff.

Unsurprisingly, London attracts significant domestic and international attention from a wide array of serious and sophisticated hotel developers, investors and operators. New

supply is a perpetual feature that broadly averages 3%-4% annual growth. Around 15,000 new rooms have opened across the capital in the past three years.

As with most other major UK city markets, IHG, Hilton, Accor, Whitbread and Travelodge are key players that continue to expand their portfolios, which currently range between 8,000 and 9,500 rooms.

However, London is far from a concentrated hotel market where only the large brands flourish. Independent hotels still account for around a quarter of the market. They are well

represented across all quality segments, ranging from two-star hotels around major railway stations such as Paddington, King's Cross St Pancras and Victoria; three-star hotels in

Bayswater and Earls Court; boutique or lifestyle hotels in vibrant social neighbourhoods such as Marylebone and Shoreditch; serviced apartments in Knightsbridge and Mayfair; and five-star luxury properties in Zone 1.

Within the larger 'brandscape', there are now 160 hotel brands operating in London and a long queue of international brands on the verge of entering or seeking to enter the

market. New overseas interest in terms of recent arrivals and imminent openings have included brands from Asia (Dorsett, Pan Pacific, Shangri-La, Tune, Wanda), Europe

(Adagio, citizenM, Qbic, ME by Melia, Motel One) and North America (Ace, Gansevoort, Hyatt Place, Morgans and Moxy).

In the past five years, the erstwhile, less-favoured London boroughs of Lambeth, Newham, Southwark and Tower Hamlets have experienced very strong growth in new hotel

openings from a relatively small base. Further growth in these areas will continue, with Hackney next to join the fray.

Over the next two years, more than 10,000 hotel rooms are due to open in London, the vast majority of which in areas that five years ago would have seemed an unlikely choice and 10 years ago virtually unthinkable.

There are a number of particular hotspots in such areas, with high levels of active new construction pipeline; over 2,000 rooms will open in the dog-leg stretch from Tower Hill up

to Aldgate and east towards Whitechapel; more than 1,000 rooms will open in the trendy area of Shoreditch and the neighbouring tech city around Old Street; and south of the river around 1,750 rooms are scheduled to open as part of the regeneration of Vauxhall/Nine Elms and Battersea.

London is undoubtedly fertile territory for hotels and it is a buoyant market that looks set to continue expanding strongly into the medium term. Supply does come out of the

market - around 35 hotels have closed in the past three years. However, the impact has been a modest 1% reduction in rooms and, in most cases, closures have tended to be driven by residential property conversion or redevelopment for an alternative use, in areas like Bayswater or Kensington, generating a superior return on capital for developers.

Alan Gordon, director, AM:PM

Resurging confidence

2014 is the year in which we have really seen the hotel market come back to life. Confidence has returned, with London transactions leading the way. This has seen trading performances strengthen and the banks' appetite to fund hotel deals (albeit with stricter conditions) return too. We have seen a large number of UK hotel portfolio deals this

year, including the sale of LRG (21 hotels), QMH (12 hotels), De Vere Hotels & Resorts and Menzies. This is in addition to single-asset sales, such as the Crowne Plaza London Ealing, the Lowry hotel in Manchester and the Grand Brighton.

We have certainly experienced an increase in competition for correctly priced assets, and this has resulted in competitive bidding scenarios that have moved sales proceeds, in some cases, in excess of 10% on clients' expectations.

Hotel owners and lenders have been keen to capitalise on the improvements in the market, and one reason for the higher sales prices is that we are seeing an increased willingness for investors to consider future trading forecasts and capital growth when estimating the attractiveness of an investment opportunity, particularly in London.

So where is the money for these investments coming from? A large proportion is predominantly from North America. Middle Eastern clients tend to focus more on the top end of the market, which by its nature is more sporadic. The hotel sector has also seen Asian and Chinese buyers and has been very active, again on a more sporadic, high-quality basis.

I believe we will continue to see overseas cash buyers hold the upper hand as investors continue to focus on central London real estate, in particular hotels. I would say that supply at the required level and quality is not meeting demand, as we are seeing large amounts of capital available.

Looking ahead to 2015, I believe that the transactional market will remain full of activity. Prices will continue to be driven by investors looking at London as a safe investment, and who are able to buy now and fund later, if at all.

We have seen faster rebound in the past 12 months or so than in previous years. We can expect to see more London hotel opportunities appear in 2015. We may also see investors who acquired assets at what was perceived to be the bottom of the market looking to exit during 2015.

Clearly UK hotel assets are in demand as this sector offers good, long-term income streams, which attract considerable interest and I would see this continuing into the foreseeable future.

David Creamore, director, hotels, Christie + Co

Tourists drive occupancy

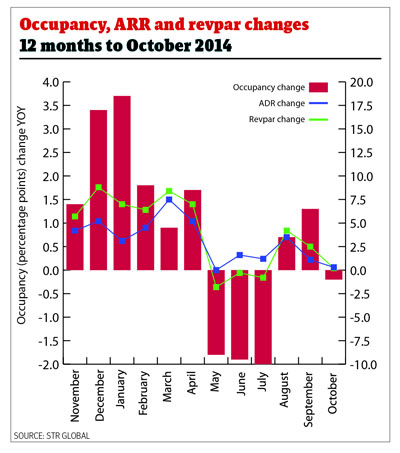

Since 2008 the London hotel industry has defied the recession and delivered modest levels of occupancy and ADR growth. However, that growth has slowed in the year to October 2014.

A surge in tourism in 2014 saw London regain its title as the world's most popular tourist destination, with the number of tourists visiting the capital increasing by 8%, according

to the Office of National Statistics. Occupancy rates of 82.8% in the year to October 2014 continue to exceed those of other major UK cities, albeit their growth rate has stagnated with a year on year increase of 0.7%.

There has been significant investment from around the world, with new openings including the Shangri-La hotel at the Shard, Hampton by Hilton at London Waterloo and

Chiltern Firehouse in Marylebone.

The London hotel market saw significant improvements between January and March, experiencing a 5% increase year on year in ADR and a 7.3% increase year on year

in revpar. However, an unexpected decline between May and July saw a 1.9% fall year on year in occupancy rates.

Future events include the Rugby World Cup, plus the opening of new developments such as Hilton London Bankside and the Admiralty Arch hotel. These openings suggest that

further growth in capacity is expected in 2015 to complement increasing demand.

Gareth Jones, partner, Mazars UK